From 1 July 2025, GST-registered businesses in Singapore will benefit from a new administrative concession introduced by the IRAS. This change allows companies to claim input tax on fringe benefits purchased from suppliers registered under the Overseas Vendor Registration (OVR) regime for invoices issued directly to the employee.

The Fringe Benefit GST Guide now provides that:

“From 1 July 2025, the above administrative concession applies when your employee contracts directly with an overseas supplier registered under the OVR regime (“OVR supplier”) for fringe benefits, such as for professional membership fees and work-related educational courses. Your company must maintain supporting documents showing that GST had been charged by the OVR supplier.”

This means:

- Where GST is charged by an OVR supplier on an invoice to your employee, your business may claim the GST as input tax.

- Conditions remain: the employee must be reimbursed, and the expense must be recognised as a business expense in your accounts.

Why This Matters

This concession is a practical recognition of how modern fringe benefits are contracted. Many overseas service providers — particularly professional bodies and education providers — will only contract in the individual employee’s name, not the company’s.

For businesses, this removes a compliance headache:

- No more worrying about whether the supplier can invoice the company directly.

- No more lost GST claims simply because of invoicing mechanics.

- Greater alignment between domestic and OVR supplier treatment.

Key Takeaway

With this change, IRAS has made it easier for GST-registered businesses to recover input tax on genuine business expenses, reflecting the realities of today’s digital and globalised economy. While a seemingly small tweak, it offers meaningful savings and streamlines compliance for companies that routinely support employees with professional memberships and training from overseas providers.

For OVR invoices that are issued to the Company, the GST remains unclaimable (there is a technical reason for it) and the Company needs to seek a refund of the GST charged from the overseas supplier by providing the Company’s GST registration number.

For those of you who are thinking of asking the OVR suppliers to start issuing invoices to your employees so that the GST can be claimed… You are on the wrong track…

I’m the GST expert. Buy me a coffee if you wish to discuss the above.

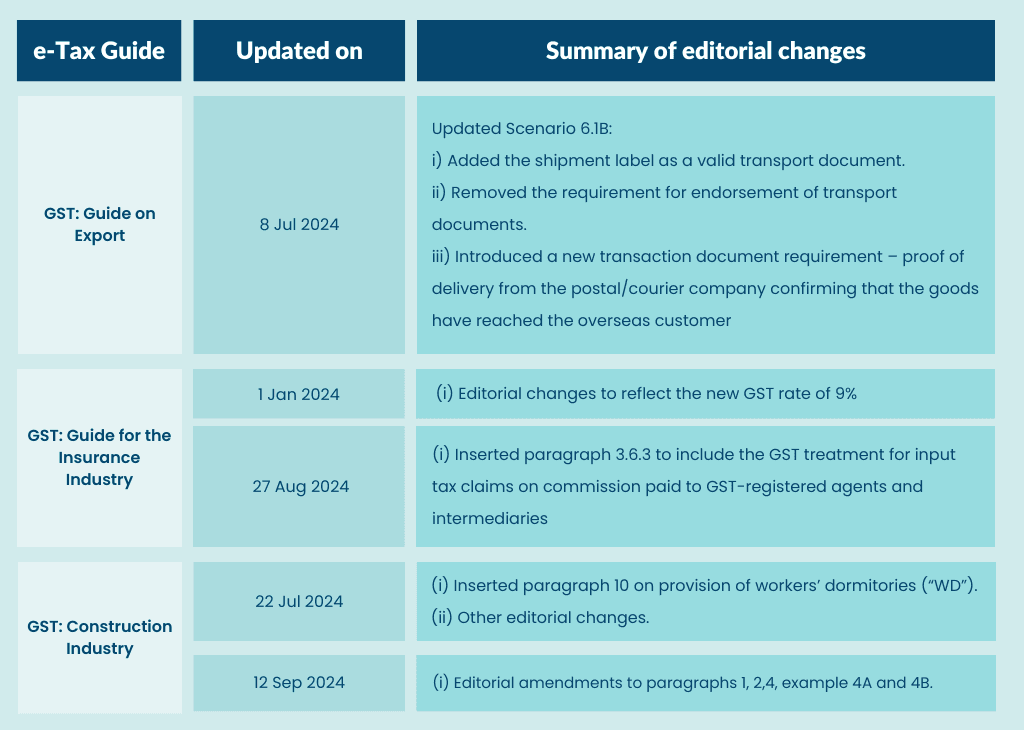

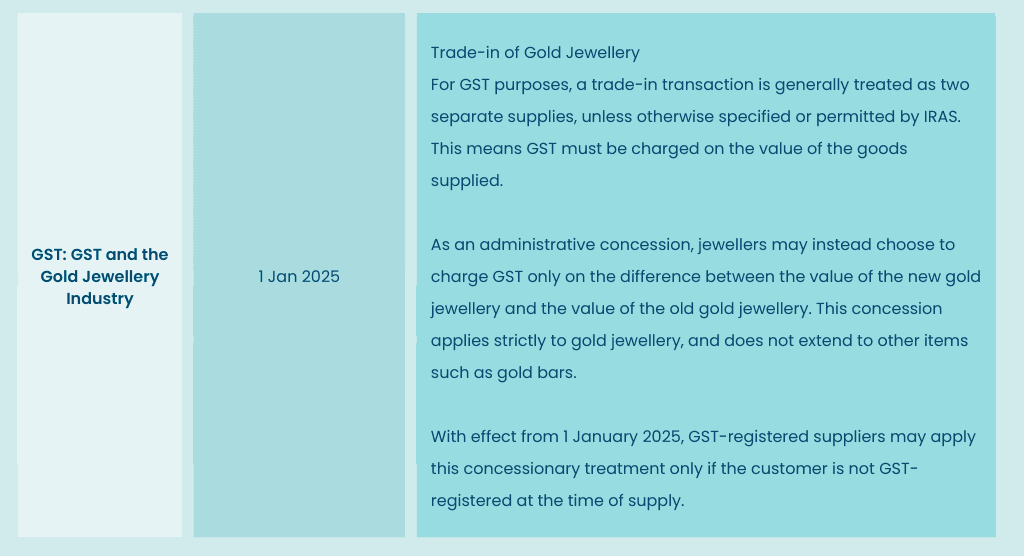

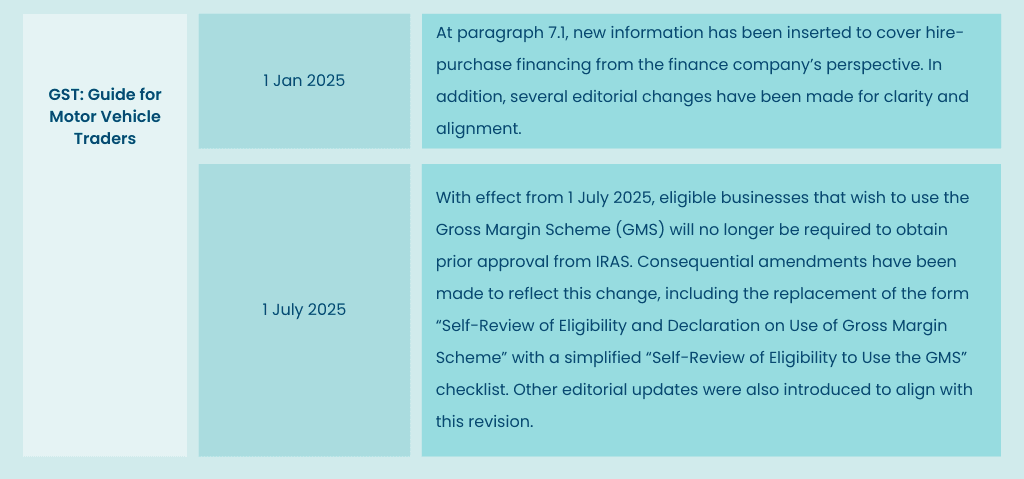

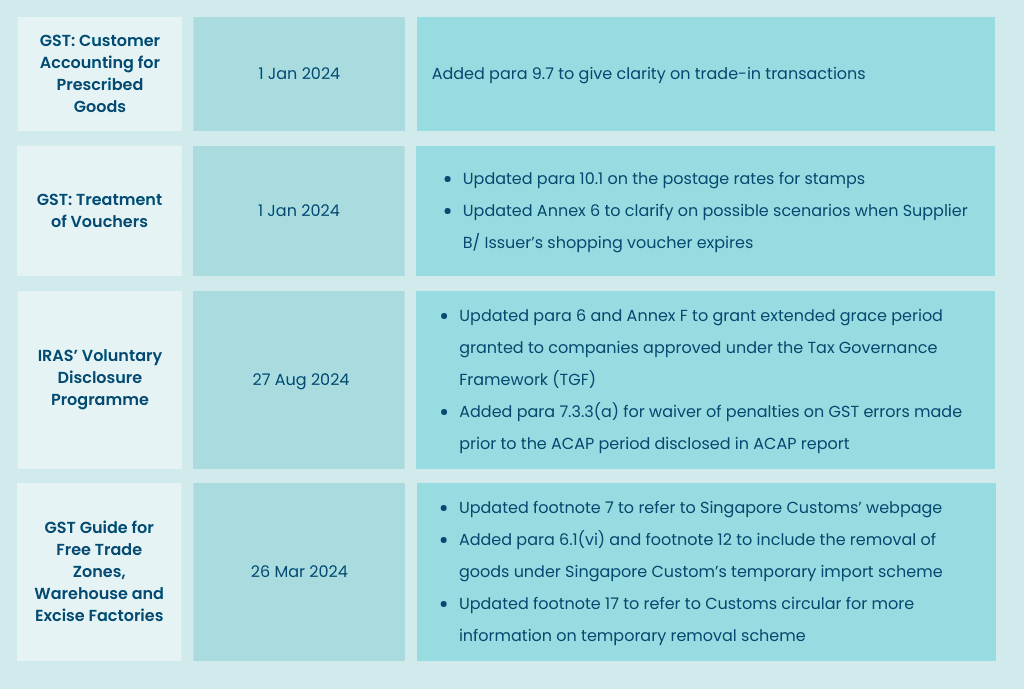

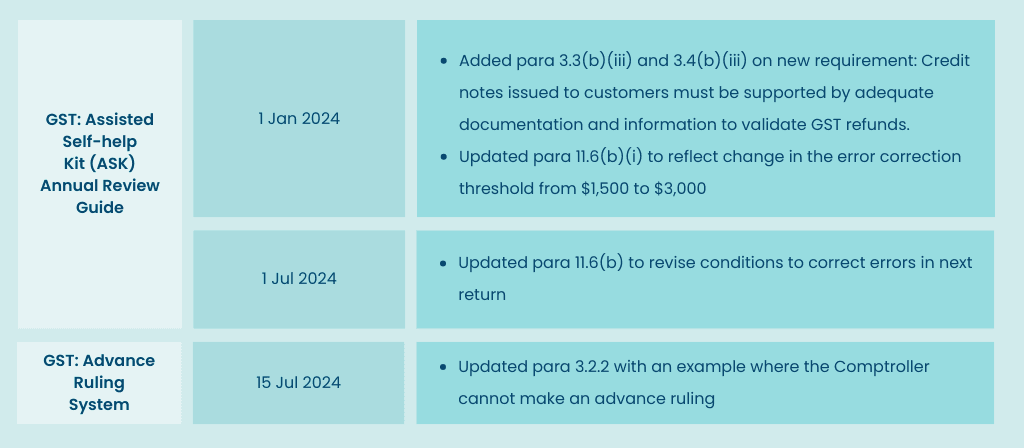

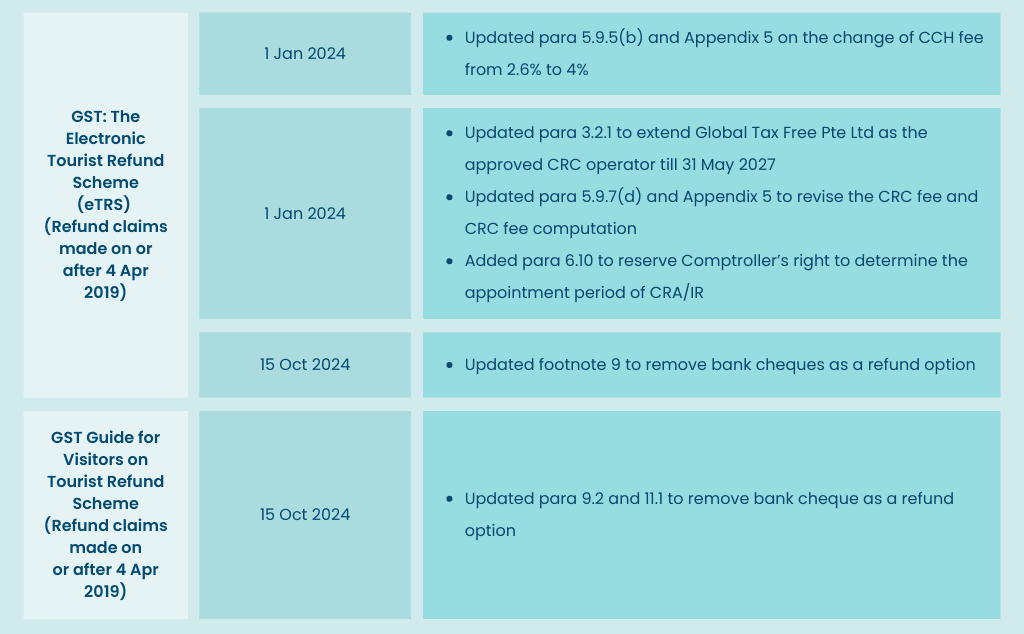

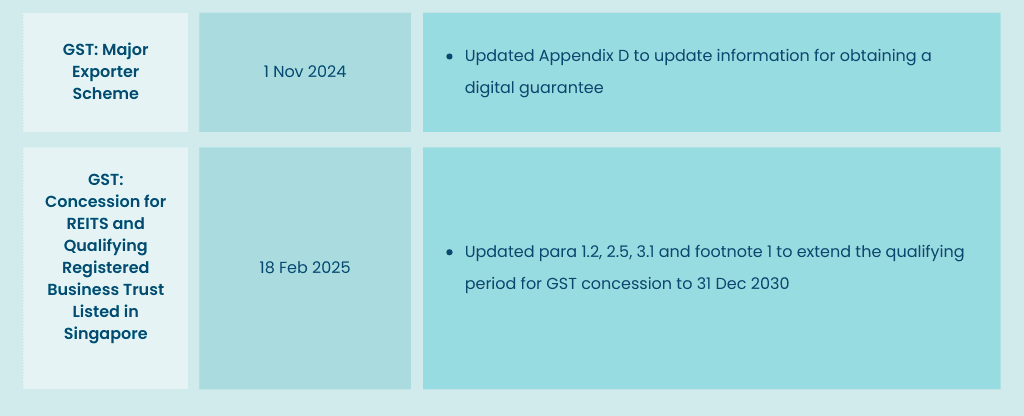

Please refer to the following table for some of the other changes to the various GST e-tax guides in 2024 and 2025.